424B3: Prospectus [Rule 424(b)(3)]

Published on April 10, 2025

|

PROSPECTUS |

Filed Pursuant to Rule 424(b)(3) |

COINCHECK GROUP N.V.

Primary Offering of

4,860,148 Ordinary Shares Underlying Warrants

Secondary Offering of

127,895,040 Ordinary Shares

129,611 Warrants to Purchase Ordinary Shares and

129,611 Ordinary Shares Underlying Warrants

This prospectus relates to the offer and sale by us of (i) up to 4,730,537 of our ordinary shares with a nominal value of one eurocent (EUR 0.01) each (“Ordinary Shares”) that are issuable by us upon the exercise of 4,730,537 Public Warrants (as defined below) that were previously registered, and (ii) up to 129,611 Ordinary Shares that are issuable by us upon the exercise of 129,611 Private Warrants (as defined below).

This prospectus also relates to the offer and sale from time to time by the selling securityholders named in this prospectus (collectively, the “Selling Securityholders”) of

(A) up to 127,895,040 Ordinary Shares, comprising

(i) up to 4,195,973 Ordinary Shares (the “TBCP Ordinary Shares”) that were issued to TBCP IV, LLC (the “Thunder Bridge Sponsor” or “Sponsor”) in exchange for (i) 3,547,918 shares of common stock of TBCP IV, LLC and (ii) 648,055 outstanding placement units held by the Thunder Bridge Sponsor that were issued in connection with the private placement that closed simultaneously with the closing of Thunder Bridge’s initial public offering pursuant to the Placement Unit Purchase Agreement, dated June 29, 2021, between Thunder Bridge and Thunder Bridge Sponsor;

(ii) up to an aggregate of 122,587,617 Ordinary Shares (the “CNCK Ordinary Shares” and, together with the TBCP Ordinary Shares, the “BCA Ordinary Shares”) received by the Coincheck Shareholders in exchange for their existing equity interests in Coincheck, Inc. in connection with the completion of the Business Combination, including (1) up to 109,097,910 Ordinary Shares that were received by Monex Group, Inc., (“Monex”) (2) up to 9,700,464 Ordinary Shares that were received by Koichiro Wada (“Koichiro Wada”), and (3) up to 3,789,243 Ordinary Shares that were received by Yusuke Otsuka (“Yusuke Otsuka” and, together with Thunder Bridge Sponsor, Monex and Koichiro Wada, the “BCA Selling Securityholders”);

(ii) up to an aggregate of 1,111,450 Ordinary Shares (the “Next Finance Acquisition Shares”) received by the former holders (the “Next Finance Shareholders”) of all of the issued and outstanding shares (the “Next Finance Shares”) of Next Finance Tech Co., a corporation under the laws of Japan (“Next Finance Tech Co.”) in exchange for their equity interests in Next Finance Tech Co., Ltd.;

(B) up to 129,611 Private Warrants, and

(C) up to 129,611 Ordinary Shares issuable upon the exercise of the Private Warrants.

We are registering the offer and sale of these securities to satisfy certain registration rights we have granted. The Selling Securityholders may offer all or part of the securities for resale from time to time through public or private transactions, at either prevailing market prices or at privately negotiated prices. These securities are being registered to permit the Selling Securityholders to sell securities from time to time, in amounts, at prices and on terms determined at the time of offering. The Selling Securityholders may sell these securities through ordinary brokerage transactions, in underwritten offerings, directly to market makers of our shares or through any other means described in the section entitled “Plan of Distribution” herein. In connection with any sales of securities offered hereunder, the Selling Securityholders, any underwriters, agents, brokers or dealers participating in such sales may be deemed to be “underwriters” within the meaning of the Securities Act of 1933, as amended, or the Securities Act. We are registering these securities for resale by the Selling Securityholders, or their donees, pledgees, transferees, distributees or other successors-in-interest selling our Ordinary Shares or Private Warrants or interests in our Ordinary Shares or Private Warrants received after the date of this prospectus from the Selling Securityholders as a gift, pledge, partnership distribution or other transfer.

All of the securities offered by the Selling Securityholders pursuant to this prospectus will be sold by the Selling Securityholders for their respective accounts. We will not receive any proceeds from the sale by the Selling Securityholders of the securities being registered hereunder. With respect to the Ordinary Shares underlying the Warrants, we will not receive any proceeds from such shares except with respect to amounts received by us upon exercise of such Warrants to the extent such Warrants are exercised for cash. Assuming the exercise of all outstanding Warrants for cash, we would receive aggregate proceeds of approximately $55.9 million. However, whether warrantholders will exercise their Warrants, and therefore the amount of cash proceeds we would receive upon exercise, is dependent upon the trading price of the Ordinary Shares. Each Warrant will become exercisable for one Ordinary Share at an exercise price of $11.50. Therefore, if and when the trading price of the Ordinary Shares is less than $11.50, we expect that warrantholders would not exercise their Warrants. The Warrants may not be or remain in the money during the period they are exercisable and prior to their expiration and, therefore, it is possible that the Warrants may not be exercised prior to their maturity, even if they are in the money, and as such, may expire worthless with minimal proceeds received by us, if any, from the exercise of Warrants. To the extent that any of the Warrants are exercised on a “cashless basis,” we will not receive any proceeds upon such exercise. As a result, we do not expect to rely on the cash exercise of Warrants to fund our operations. Instead, we intend to rely on other sources of cash discussed elsewhere in this prospectus to continue to fund our operations. See “Use of Proceeds” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources.”

Our Ordinary Shares and Public Warrants are listed on the Nasdaq Global Market (“Nasdaq”) under the symbols “CNCK” and “CNCKW,” respectively. Holders of Ordinary Shares and Public Warrants should obtain current market quotations for their securities. On April 8, 2025, the last reported sale prices for our Ordinary Shares and Public Warrants on Nasdaq were $4.37 per share and $0.49 per warrant, respectively.

The securities being registered for resale pursuant to this prospectus include Ordinary Shares and Private Warrants that were purchased at prices or received for consideration that may be significantly below the current trading prices of these securities on the open market, and the sale of which would result in certain Selling Securityholders realizing a significant gain. The BCA Selling Securityholders acquired the BCA Ordinary Shares covered by this prospectus at average prices ranging from ¥18.86 ($0.13) per Ordinary Share to $1.55 (¥226.25) per Ordinary Share. By comparison, the offering price to public shareholders in Thunder Bridge’s initial public offering was $10.00 per unit, which consisted of one Ordinary Share and one fifth of one Public Warrant. Consequently, certain BCA Selling Securityholders may realize a positive rate for return on the sale of their Ordinary Shares covered by this prospectus even if the market price of the Ordinary Shares is below $10.00 per Ordinary Share.

The securities being registered hereby (excluding the Next Finance Acquisition Shares) were acquired in connection with the Business Combination in exchange for equity interests held in either Coincheck, Inc. or the Sponsor, or for Private Placement Units purchased pursuant to the Placement Unit Purchase Agreement. The purchase prices paid by the BCA Selling Securityholders for the Ordinary Shares were calculated based on the sum total consideration each BCA Selling Securityholders paid for such exchanged equity interest or Private Placement Units in the amount as follow: (i) Monex Group, Inc. received 109,097,910 Ordinary Shares for an effective aggregate purchase price of ¥8,356,278,855 ($57,262,241), or ¥76.59 ($0.52) per share, based on consideration paid for the exchanged equity interest held in Coincheck, Inc., (ii) Koichiro Wada received 9,700,464 Ordinary Shares for an effective aggregate purchase price of ¥16,720,000 ($2,170,356), or ¥32.65 ($0.22) per share, based on consideration paid for the exchanged equity interest held in Coincheck, Inc., (iii) Yusuke Otsuka received 3,789,243 Ordinary Shares for an effective aggregate purchase price of ¥71,482,500 ($489,841), or ¥18.86 ($0.13) per share, based on consideration paid for the exchanged equity interest held in Coincheck, Inc. and (iv) the Sponsor received 4,195,973 Ordinary Shares (excluding 2,365,278 Ordinary Shares which the Sponsor received but forfeited and surrendered for no consideration) for an effective purchase price of $6,505,560 (¥949,356,371), or $1.55 (¥226.25) per share, based on consideration paid for the exchanged equity interest held in the Sponsor. The Sponsor also received 129,611 Private Warrants exercisable at $11.50 per share underlying its Private Placement Units.

Given the lower purchase prices that the BCA Selling Securityholders paid to acquire Ordinary Shares or Warrants compared to the current trading price of our Ordinary Shares or Warrants, these BCA Selling Securityholders are likely to earn a positive rate of return on their investment at current market prices. Based on the last reported sale price on April 8, 2025 of $4.37 (¥637.71) per Ordinary Share, the BCA Selling Securityholders would realize profits on the sale of their holdings as follows: (i) Monex Group would realize a potential profit

of ¥62,447,031,929 ($427,924,566), or ¥572.39 ($3.92) per share, (ii) Koichiro Wada would realize a potential profit of ¥5,978,771,521 ($40,970,133), or ¥616.34 ($4.22) per share, (iii) Yusuke Otsuka would realize a potential profit of ¥2,387,693,389 ($16,361,909), or ¥630.12 ($4.32) per share and (iv) the Sponsor would realize a potential aggregate profit of $11,830,842 (¥1,726,474,773), or $2.82 (¥411.52), per share. The Sponsor would also realize a value of $63,276 (¥$9,233,880) upon the sale of its Private Warrants based on the April 8, 2025 last reported sale price of $0.49 (¥71.51) of our Public Warrants. The aggregate amount of profit for such BCA Selling Securityholders would be ¥72,549,205,479 ($497,150,726). Investors who purchase our Ordinary Shares in the open market may not experience a similar rate of return on the securities they purchase due to differences in the purchase prices and the current trading price.

The Ordinary Shares being registered for resale in this prospectus represent a substantial percentage of our public float and of our outstanding Ordinary Shares. The Ordinary Shares being offered for resale by the Selling Securityholders pursuant to this prospectus represent approximately 94.3% of our total outstanding Ordinary Shares as of April 8, 2025 on a fully diluted basis (assuming and after giving effect to the issuance of Ordinary Shares upon exercise of all outstanding Warrants). Once the registration statement that includes this prospectus is effective and during such time as it remains effective, the Selling Securityholders will be permitted (subject to compliance with the contractual lock-up restrictions that apply to certain Selling Securityholders, as described under “Shares Eligible for Future Sale”) to sell the shares registered hereby. Based on the last reported sale price of our Ordinary Shares on April 8, 2025, BCA Selling Securityholders may realize profit per share ranging from ¥411.46 ($2.82) to ¥618.85 ($4.24), even though the current trading price of our Ordinary Shares is below the $10.00 offering price to public shareholders in Thunder Bridge’s initial public offering. The resale, or anticipated or potential resale, of a substantial number of shares of our Ordinary Shares may have a material negative impact on the market price of our Ordinary Shares and could make it more difficult for our shareholders to sell their Ordinary Shares at such times and at such prices as they deem desirable. Additionally, even if the price of our Ordinary Shares declines substantially, some Selling Securityholders may still have an incentive to sell to obtain liquidity.

We will bear all costs, expenses and fees in connection with the registration of the securities offered by this prospectus, including, without limitation, all registration and filing fees (including fees with respect to filings required to be made with FINRA (as defined herein)), Nasdaq listing fees, fees and expenses of compliance with securities or blue sky laws, if any, and fees and expenses of counsel and independent registered public accountants, whereas the Selling Securityholders will bear all incremental selling expenses, including commissions and discounts, brokerage fees, underwriting marketing costs, legal counsel fees that are not covered by us and any other expenses incurred by the Selling Securityholders in disposing of the securities, as described in the section entitled “Plan of Distribution.”

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read this entire prospectus and any amendments or supplements carefully before you make your investment decision.

We are a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company disclosure and reporting requirements. See “Prospectus Summary — Implications of Being a Foreign Private Issuer and a Controlled Company.”

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 13 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities.

Neither the U.S. Securities and Exchange Commission, or SEC, nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

PROSPECTUS DATED APRIL 8, 2025

|

Page |

||

|

ii |

||

|

iii |

||

|

v |

||

|

v |

||

|

v |

||

|

vi |

||

|

viii |

||

|

1 |

||

|

10 |

||

|

13 |

||

|

58 |

||

|

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

59 |

|

|

NOTES TO THE UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

65 |

|

|

67 |

||

|

68 |

||

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION |

69 |

|

|

97 |

||

|

132 |

||

|

140 |

||

|

141 |

||

|

143 |

||

|

146 |

||

|

158 |

||

|

160 |

||

|

174 |

||

|

176 |

||

|

177 |

||

|

177 |

||

|

ENFORCEABILITY OF CIVIL LIABILITIES AND AGENT FOR SERVICE OF PROCESS |

177 |

|

|

177 |

||

|

F-1 |

You should rely only on the information contained or incorporated by reference in this prospectus or any supplement. Neither we nor the Selling Securityholders have authorized anyone else to provide you with different information. The securities offered by this prospectus are being offered only in jurisdictions where the offer is permitted. You should not assume that the information in this prospectus or any supplement is accurate as of any date other than the date on the front of each document. Our business, financial condition, results of operations and prospects may have changed since that date.

Except as otherwise set forth in this prospectus, neither we nor the Selling Securityholders have taken any action to permit a public offering of these securities outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of these securities and the distribution of this prospectus outside the United States.

i

This prospectus is part of a registration statement on Form F-1 that we filed with the SEC. The Selling Securityholders named in this prospectus may, from time to time, sell the securities described in this prospectus in one or more offerings. This prospectus includes important information about us, the securities being offered by the Selling Securityholders and other information you should know before investing. Any prospectus supplement may also add, update, or change information in this prospectus. If there is any inconsistency between the information contained in this prospectus and any prospectus supplement, you should rely on the information contained in that particular prospectus supplement. This prospectus does not contain all of the information provided in the registration statement that we filed with the SEC. You should read this prospectus together with the additional information about us described in the section below entitled “Where You Can Find Additional Information.” You should rely only on information contained in this prospectus and any prospectus supplement. We have not, and the Selling Securityholders have not, authorized anyone to provide you with information different from that contained in this prospectus and any prospectus supplement. The information contained in this prospectus is accurate only as of the date on the front cover of this prospectus. You should not assume that the information contained in this prospectus is accurate as of any other date.

The Selling Securityholders may offer and sell the securities directly to purchasers, through agents selected by the Selling Securityholders, or to or through underwriters or dealers. A prospectus supplement, if required, may describe the terms of the plan of distribution and set forth the names of any agents, underwriters or dealers involved in the sale of securities. See “Plan of Distribution.”

Throughout this prospectus, unless otherwise designated or the context requires otherwise, the terms “we,” “us,” “our,” “Coincheck Group,” “the Company” and “our company” refer to Coincheck Group N.V. and its subsidiaries, which prior to the Business Combination was the business of Coincheck, Inc. (“Coincheck”).

ii

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Statements

Coincheck Group N.V.

Following the Business Combination, we qualified as a Foreign Private Issuer and prepare our financial statements in accordance with International Financial Reporting Standards (“IFRS”) Accounting Standards, as issued by the International Accounting Standards Board (“IASB”). The unaudited condensed consolidated interim financial statements of the Company as of December 31, 2024 and for the three and nine months ended December 31, 2023 and 2024 have been prepared in accordance with International Accounting Standards (“IAS”) 34 “Interim Financial Reporting” as issued by IASB and in its presentation and reporting currency of Japanese yen (“¥”).

Coincheck, Inc.

The audited financial statements of Coincheck, Inc. as of and for the fiscal years ended March 31, 2022, 2023 and 2024 have been prepared in accordance with IFRS Accounting Standards as issued by IASB and in its presentation and reporting currency of Japanese yen.

Thunder Bridge Capital Partners IV, Inc.

The historical audited financial statements of Thunder Bridge Capital Partners IV, Inc. (“Thunder Bridge”) as of and for the year ended December 31, 2023 and 2022 and the unaudited condensed interim financial statements of Thunder Bridge as of and for the three and nine months ended September 30, 2024 have been prepared in accordance with the generally accepted accounting principles in the United States (“U.S. GAAP”) and in its presentation and reporting currency of U.S. dollars (“USD”).

Accounting Treatment of the Business Combination

The Business Combination has been accounted for as a reverse recapitalization. Under this method of accounting, Thunder Bridge has been treated as the “acquired” company for financial reporting purposes. Accordingly, the Business Combination has been treated as the equivalent of Coincheck issuing shares at the consummation of the Business Combination (the “Closing”) for the net assets of Thunder Bridge as of December 10, 2024 (the “Closing Date”), accompanied by a recapitalization. The net assets of Thunder Bridge have been stated at fair value, with no goodwill or other intangible assets recorded.

This determination was primarily based on the fact that the existing Coincheck stockholders have a majority of the voting power of the Company.

The Business Combination is not within the scope of IFRS 3 since there is no change in control based on the continued control of the Company by existing Coincheck stockholders and Thunder Bridge does not meet the definition of a business in accordance with IFRS 3; as such, the Business Combination has been accounted for within the scope of IFRS 2. Any excess of fair value of Coincheck shares issued over the fair value of Thunder Bridge’s identifiable net assets acquired represents compensation for the service of a stock exchange listing for its shares and is expensed as incurred.

Basis of Pro Forma Presentation

The historical financial information has been adjusted to give pro forma effect to the transaction accounting required for the Business Combination as per the Business Combination Agreement. The adjustments in the unaudited pro forma condensed combined financial information have been identified and presented to provide relevant information necessary for an accurate understanding of the combined entity upon the Closing. The unaudited pro forma condensed combined financial information has been presented for illustrative purposes only and is not necessarily indicative of the financial position and results of operations that would have been achieved had the Business Combination and related transactions occurred on the dates indicated. Further, the unaudited pro forma condensed combined financial information may not be useful in predicting the future financial condition and results of operations of the Company. The actual financial position and results of operations may differ significantly from the pro forma amounts reflected herein due to a variety of factors. The unaudited pro forma adjustments

iii

represent management’s estimates based on information available as of the date of these unaudited pro forma condensed combined financial statements and are subject to change as additional information becomes available and analyses are performed. Coincheck and Thunder Bridge have not had any historical relationship prior to the Business Combination. Accordingly, no pro forma adjustments were required to eliminate activities between the companies.

The adjustments presented on the pro forma combined financial statements have been identified and presented to provide an understanding of the Company upon consummation of the Business Combination for illustrative purposes only. The financial results may have been different had the companies always been combined for the historical periods presented here. You should not rely on the pro forma combined financial statements as being indicative of the future financial position and results that the Company will experience.

Non-IFRS Financial Measures

In addition to our results determined in accordance with IFRS, we present EBITDA and Adjusted EBITDA, non-IFRS measures, because we believe they are useful in evaluating our operating performance. EBITDA represents net profit (loss) for the period before the impact of taxes, interest, depreciation, and amortization of intangible assets, and Adjusted EBITDA represents EBITDA, further adjusted for transaction expenses that are directly attributable to the Reverse Recapitalization, as well as Nasdaq listing expenses.

We use EBITDA and Adjusted EBITDA to evaluate our ongoing operations and for internal planning and forecasting purposes. We believe that EBITDA and Adjusted EBITDA may be helpful to investors because it provides consistency and comparability with past financial performance. However, EBITDA and Adjusted EBITDA are presented for supplemental informational purposes only, have limitations as an analytical tool and should not be considered in isolation or as a substitute for our financial information presented in accordance with IFRS.

Rounding

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

Fiscal Year

Our fiscal year begins on April 1 and ends on March 31 of the following year.

iv

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

We have proprietary rights to trademarks used in this prospectus that are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the “®” or “TM” symbols, but the lack of such symbols is not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. The use or display herein of other companies’ trademarks, trade names or service marks is not intended to imply a relationship with, or endorsement or sponsorship of us by, any other companies, or a sponsorship or endorsement of any such other companies by us. Each trademark, trade name or service mark of any other company appearing in this prospectus is the property of its respective holder.

This prospectus contains translations of certain U.S. dollar amounts into Japanese yen, and Japanese yen amounts into U.S. dollars, solely for the convenience of the reader. Such translations were made at the rate of $1.00 to ¥145.93 (or ¥1000 to $6.85), which was the foreign exchange rate on April 4, 2025 as reported by the Board of Governors of the Federal Reserve System in its weekly release on April 7, 2025. Historical and current exchange rate information may be found at https://www.federalreserve.gov/releases/h10/. Such currency amounts are not necessarily indicative of the amounts of currency that could actually have been purchased upon exchange of Japanese yen or U.S. dollars at the dates indicated or any other date, and, when expressed in Japanese yen or U.S. dollars in the future, such amounts may be different from those set forth in this prospectus due to intervening exchange rate fluctuations.

Market data and certain industry forecast data used in this prospectus were obtained from internal reports, where appropriate, as well as third-party sources, including independent industry publications, as well as other publicly available information. Data regarding the industries in which we compete and our market position and market share within these industries are inherently imprecise and are subject to significant business, economic and competitive uncertainties beyond our control, but we believe they generally indicate size, position and market share. In addition, assumptions and estimates of our and our industries’ future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors. These and other factors could cause our future performance to differ materially from our assumptions and estimates. As a result, you should be aware that market, ranking and other similar industry data included in this prospectus, and estimates and beliefs based on that data, may not be reliable. See “Cautionary Statement Regarding Forward-Looking Statements.”

v

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. These forward-looking statements relate to expectations for future financial performance, business strategies or expectations for our business. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking.

These forward-looking statements are based on information available as of the date of this prospectus and our managements’ current expectations, forecasts and assumptions, and involve a number of judgments, known and unknown risks and uncertainties and other factors, many of which are outside of our control. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date. We do not undertake any obligation to update, add or to otherwise correct any forward-looking statements contained herein to reflect events or circumstances after the date they were made, whether as a result of new information, future events, inaccuracies that become apparent after the date hereof or otherwise, except as may be required under applicable securities laws.

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this prospectus. As a result of a number of known and unknown risks and uncertainties, actual results or performance may be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in this prospectus under “Risk Factors” and the following:

• a delay or failure to realize the expected benefits from the Business Combination;

• the price of crypto assets and volume of transactions on Coincheck’s platform;

• the development, utility and usage of crypto assets;

• changes in economic conditions and consumer sentiment in Japan;

• cyberattacks and security breaches on the Coincheck platform;

• demand for any particular crypto asset;

• adverse changes to any laws or regulations in the United States, Japan or the Netherlands or Coincheck’s failure to comply with any laws or regulations;

• administrative sanctions, including fines, or legal claims if we are found to have offered services in violations of the laws of jurisdictions other than Japan or to have violated international sanctions regimes;

• Coincheck’s ability to compete in a highly competitive industry;

• Coincheck’s ability to introduce new products and services;

• any interruptions in services provided by third-party service providers;

• the status of any particular crypto asset as a “security” in any relevant jurisdiction;

• legal, regulatory, and other risks in connection with our operation of Coincheck NFT Marketplace that could adversely affect our business, operating results, and financial condition;

• our obligations to comply with the laws, rules, regulations, and policies of a variety of jurisdictions if we expand our international activities;

• the inability to maintain the listing of our Ordinary Shares on Nasdaq;

vi

• the ability to grow and manage growth profitably; and

• other risks and uncertainties indicated in this prospectus, including those set forth under the section entitled “Risk Factors.”

Should one or more of these risks or uncertainties materialize or should any of the assumptions made by our management prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this prospectus. All forward-looking statements included herein are expressly qualified in their entirety by the cautionary statements contained or referred to in this section as well as any other cautionary statements contained herein. In light of these risks and uncertainties, you should keep in mind that any event described in a forward-looking statement made in this prospectus or elsewhere might not occur.

vii

The following terms used in this prospectus have the meanings indicated below:

|

Term |

Description |

|

|

Address |

An alphanumeric reference to where crypto assets can be sent or stored. |

|

|

Bitcoin (“BTC”) |

The first system of global, decentralized, scarce, digital money as initially introduced in a white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System” by Satoshi Nakamoto. |

|

|

Block |

Synonymous with digital pages in a ledger. Blocks are added to an existing blockchain as transactions occur on the network. Miners are rewarded for “mining” a new block. |

|

|

Blockchain |

A cryptographically secure digital ledger that maintains a record of all transactions that occur on the network and follows a consensus protocol for confirming new blocks to be added to the blockchain. |

|

|

Board or Board of Directors |

The board of directors of Coincheck Group N.V. |

|

|

Business Combination |

The Business Combination consummated on December 10, 2024, pursuant to the Business Combination Agreement. |

|

|

Business Combination Agreement |

The Business Combination Agreement, dated as of March 22, 2022, as amended from time to time, by and among Thunder Bridge, Coincheck Group B.V., a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) (which was converted into a Dutch public limited liability company (naamloze vennootschap) and renamed Coincheck Group N.V. immediately prior to the Business Combination), M1 GK, Merger Sub and Coincheck. |

|

|

Coincheck |

Coincheck, Inc., a Japanese joint stock company (kabushiki kaisha). |

|

|

Coincheck Parent |

Coincheck Group N.V., a Dutch public limited liability company (naamloze vennootschap) (which was Coincheck Group B.V., a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) prior to its conversion in connection with the Business Combination.) |

|

|

Coincheck Shareholders |

Monex Group, Inc., Koichiro Wada and Yusuke Otsuka. |

|

|

Coincheck NFT Marketplace |

Coincheck’s service that enables non-fungible tokens to be traded between users or purchased by users from Coincheck. |

|

|

Cold storage/Cold wallet |

The storage of private keys in any fashion that is disconnected from the internet in order to protect data from unauthorized access. Common cold storage examples include offline computers, USB drives or paper records. |

|

|

Cover counterparties |

Counterparties with which cover transactions are executed. |

|

|

Cover transactions |

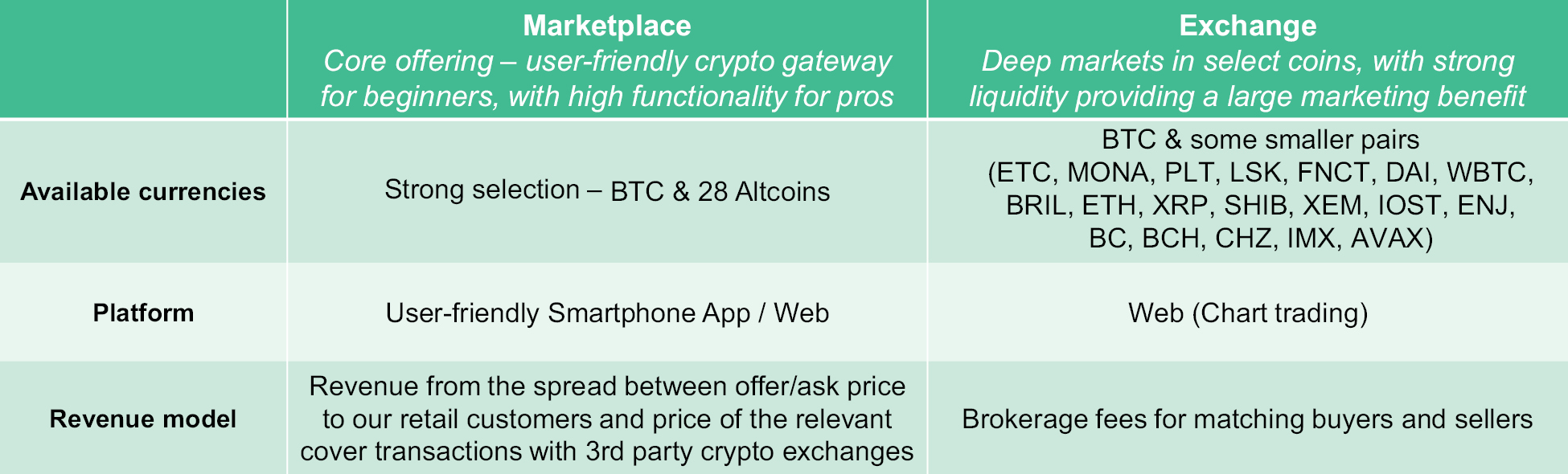

Transactions executed by Coincheck on an external exchange or on Coincheck’s Exchange platform in order to hedge Coincheck’s own position arising from transactions in crypto assets with users of Coincheck’s Marketplace platform. |

|

|

Crypto |

A broad term for any cryptography-based market, system, application, or decentralized network. |

viii

|

Term |

Description |

|

|

Crypto asset (or “token”) |

A digital asset built using blockchain technology, including cryptocurrencies and NFTs. Under Japan’s Payment Services Act, digital assets that constitute a “security token” (i.e., electronically recorded transferable rights (“ERTRs”) or electronically recorded transferable rights to be indicated on securities (“ERTRISs”) under Japan’s Financial Instruments and Exchange Act (“FIEA”)) are excluded from the definition of crypto assets. Accordingly, crypto assets consist only of digital assets that have been determined not to constitute ERTRs or ERTRISs. |

|

|

Cryptocurrency |

Bitcoin and alternative coins, or “altcoins,” launched after the success of Bitcoin. This category of crypto asset is designed to work as a medium of exchange, store of value, or to power applications and excludes security tokens. |

|

|

Customer assets (IFRS) |

Safeguard liabilities + fiat currency deposited by customers on IFRS basis. |

|

|

Customers (or “users”) |

Parties who hold accounts and utilize the services provided on crypto asset platforms. This definition, as used in the description of our business, generally does not include cover counterparties, and thus such definition differs from the definition of “customer” under IFRS 15. Notwithstanding the foregoing, for purposes of Coincheck’s audited financial statements and the Company’s condensed interim consolidated financial statements included elsewhere in this prospectus, “customers” refers to customers that meet the definition of a customer under IFRS 15, including the parties described in the preceding paragraph as well as cover counterparties. |

|

|

DeFi |

Short for “Decentralized Finance,” referring to a peer-to-peer software-based network of protocols that can be used to facilitate traditional financial services like borrowing, lending, trading derivatives, insurance and more through smart contracts. |

|

|

Ethereum (“ETH”) |

A decentralized global computing platform that supports smart contract transactions and peer-to-peer applications, or “Ether,” the native crypto assets on the Ethereum network. |

|

|

Exchange Act |

The U.S. Securities Exchange Act of 1934, as amended. |

|

|

Exchange platform |

Coincheck’s exchange platform on which Coincheck mediates transactions between users selling and users purchasing 20 different types of cryptocurrencies as of December 31, 2024 and transacts to facilitate Coincheck’s cover transactions. |

|

|

FEFTA |

The Foreign Exchange and Foreign Trade Act of Japan (Act No. 228 of 1948). Under FEFTA, Japan’s Ministry of Finance and its ministries with jurisdiction over a target entity’s business review foreign direct investments and impose certain restrictions on such investments made by foreign investors. |

|

|

Fork |

A fundamental change to the software underlying a blockchain which results in two different blockchains, the original, and the new version. In some instances, the fork results in the creation of a new token. |

|

|

Hot wallet |

A wallet that is connected to the Internet, enabling it to broadcast transactions. |

ix

|

Term |

Description |

|

|

Initial Exchange Offering (“IEO”)/Initial Token Offering |

|

|

|

Japan Virtual and Crypto assets Exchange Association (the “JVCEA”) |

|

|

|

M1 GK |

M1 Co G.K., a Japanese limited liability company (godo kaisha) |

|

|

Marketplace platform |

As of December 31, 2024, Coincheck’s platform that supports 29 different types of cryptocurrencies and enables users to trade cryptocurrencies with Coincheck in yen or with other cryptocurrencies. |

|

|

Marketplace platform business |

Coincheck’s business is related to the Marketplace platform, where Coincheck buys and sells crypto assets to users on the Marketplace platform and executes cover transactions on an external exchange or Coincheck’s Exchange platform for the purpose of hedging Coincheck’s own position. |

|

|

Merger Sub |

Coincheck Merger Sub Inc., a Delaware corporation and a wholly-owned subsidiary of Coincheck Parent. |

|

|

Miner |

Individuals or entities who operate a computer or group of computers that add new transactions to blocks and verify blocks created by other miners. Miners collect transaction fees and are rewarded with new tokens for their service. |

|

|

Mining |

The process by which new blocks are created, and thus new transactions are added to the blockchain. |

|

|

Monex |

Monex Group, Inc., a Japanese joint stock company (kabushiki kaisha) listed on the Tokyo Stock Exchange. |

|

|

Nasdaq |

Nasdaq Global Market. |

|

|

NEM (“XEM”) |

NEM (abbreviated as “XEM” on exchange platforms) is a type of open-source cryptocurrency developed for the “New Economic Movement” network. NEM is a crypto asset with a strong community in Japan in particular, and the goal of NEM is to establish a new economic framework based on the principles of decentralization, economic freedom and equality rather than the existing frameworks managed by countries and governments. |

|

|

Network |

The collection of all miners that use computing power to maintain the ledger and add new blocks to the blockchain. Most networks are decentralized, which reduce the risk of a single point of failure. |

x

|

Term |

Description |

|

|

Non-fungible token (“NFT”) |

A unique and non-interchangeable unit of data stored on a blockchain which allows for a verified and public proof of ownership, first launched on the Ethereum blockchain. |

|

|

Off-chain |

A type of transaction that is not directly recorded on a blockchain. |

|

|

On-chain |

A type of transaction that is directly recorded as data on a blockchain. |

|

|

Protocol |

A type of algorithm or software that governs how a blockchain operates. |

|

|

Public key or private key |

Each public address has a corresponding public key and private key that are cryptographically generated. A private key allows the recipient to access any funds belonging to the address, similar to a bank account password. A public key helps validate transactions that are broadcasted to and from the address. Addresses are shortened versions of public keys, which are derived from private keys. |

|

|

SEC |

The U.S. Securities and Exchange Commission. |

|

|

Securities Act |

The U.S. Securities Act of 1933, as amended. |

|

|

Security token |

A security using encryption technology. This includes digital forms of traditional equity or fixed income securities, or may be assets deemed to be a security based on their characterization as an investment contract or note. |

|

|

Smart contract |

Software that digitally facilitates or enforces a rules-based agreement or terms between transacting parties. |

|

|

Stablecoin |

Crypto assets designed to minimize price volatility. A stablecoin is designed to track the price of an underlying asset such as fiat money or an exchange-traded commodity (such as precious metals or industrial metals). Stablecoins can be backed by fiat money or other crypto assets. |

|

|

UI |

Short for “user interface design,” referring to a human-first approach to product design that focuses on the effectiveness of products. |

|

|

US$ or $ |

Refers to U.S. dollars. |

|

|

UX |

Short for “user experience design,” referring to a human-first approach to product design that focuses on the aesthetic experience of products. |

|

|

Wallet |

A place to store public and private keys for crypto assets. Wallets are typically software, hardware or paper records. |

xi

This summary highlights certain information about us, this offering and selected information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before deciding whether to invest in the securities covered by this prospectus. You should read the following summary together with the more detailed information in this prospectus, including the information set forth in the section titled “Risk Factors” in this prospectus in their entirety before making an investment decision.

Overview

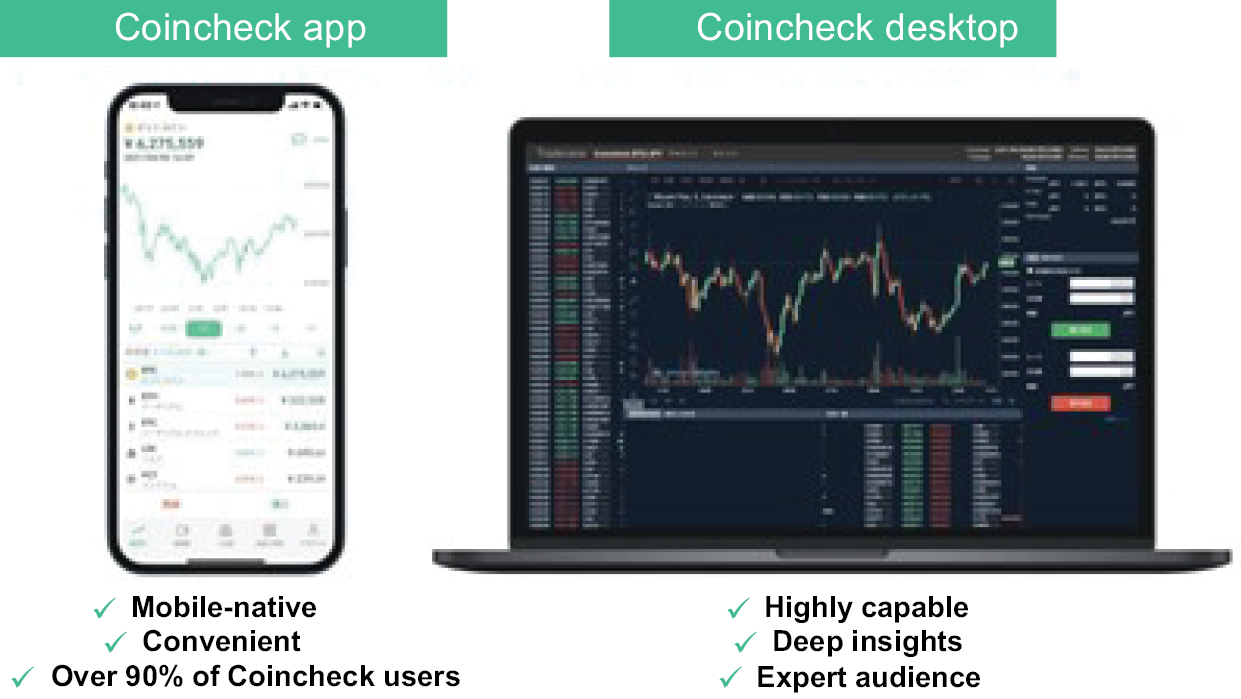

We operate one of the largest multi-cryptocurrency marketplaces and exchanges in Japan and are regulated by the JFSA. We are a leader in the Japanese crypto exchange industry, providing Marketplace and Exchange platforms on which diverse cryptocurrencies, including Bitcoin and Ethereum, are held and exchanged, and offering other retail-focused crypto services. We are also increasing Japanese users’ access to innovative digital products and solutions beyond cryptocurrencies, such as non-fungible tokens (“NFTs”), and seek to enable Japanese users to access the benefits of emerging new technologies. We believe we are well positioned to benefit from increasing adoption of cryptocurrencies and other new technologies within the world’s fourth largest economy.

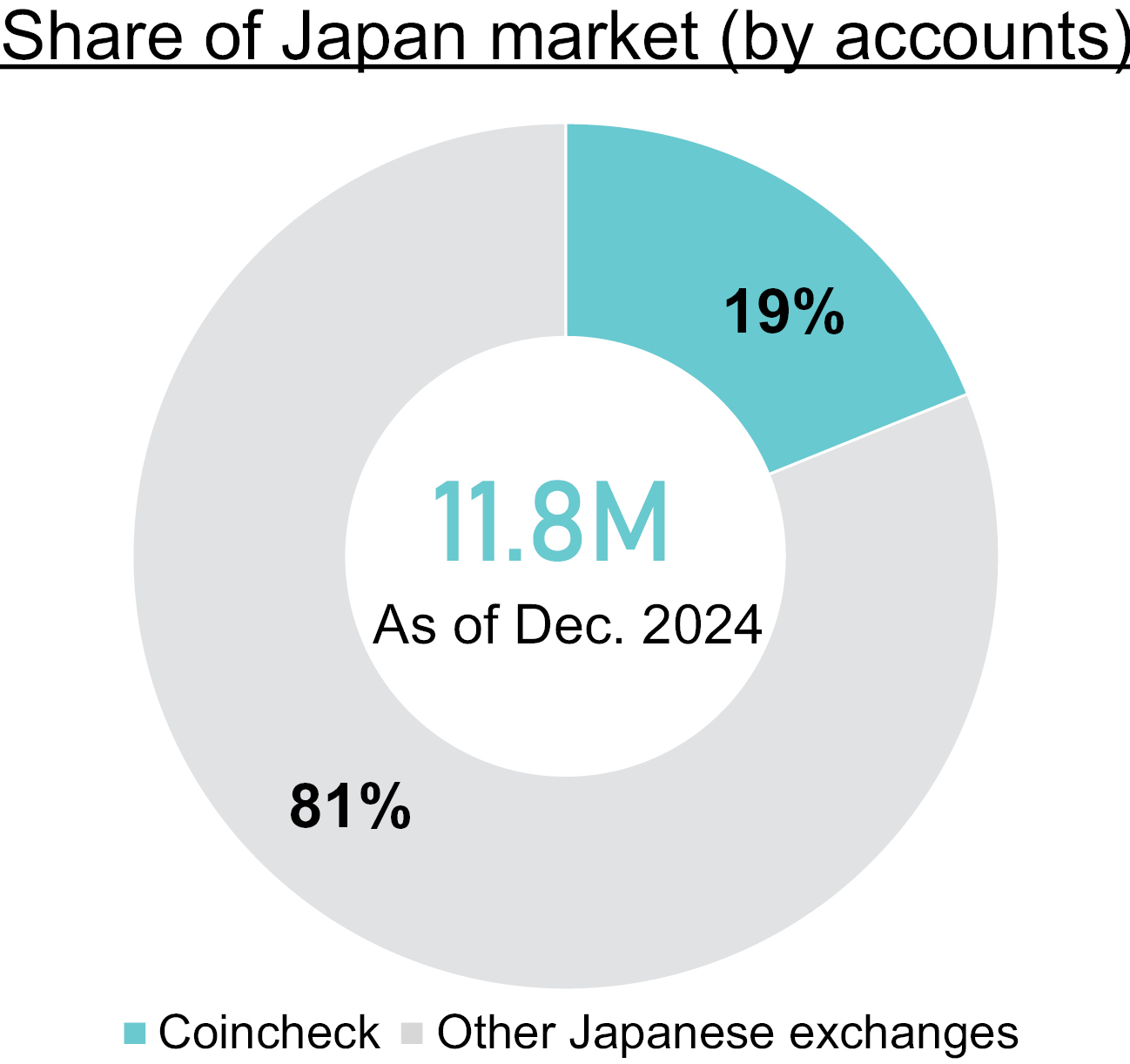

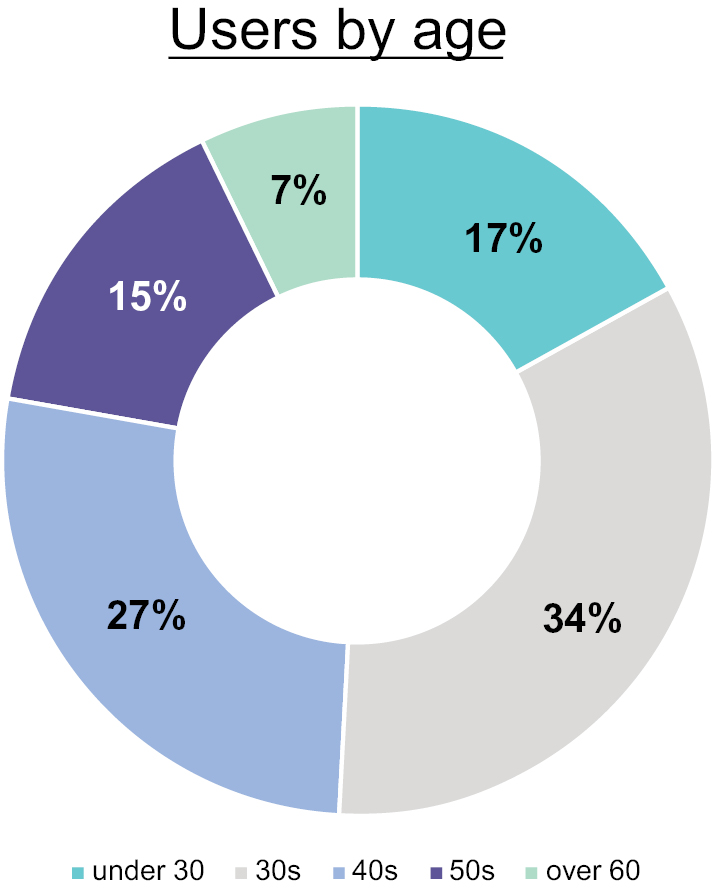

We estimate that 18.6% of cryptocurrency users in Japan have a verified Coincheck account, or approximately 2.2 million users as of December 31, 2024, based on data compiled by the JVCEA. We believe that our users choose us due to our trusted and recognized brand, robust product offering and strong customer service. Approximately 51% of these accounts are held by customers under 40 as of December 31, 2024, providing the opportunity for our business to grow alongside our customers as they reach their prime earning years. We believe that this, combined with our constant innovation and robust KYC/AML and compliance infrastructure, positions us to capitalize on the potential growth of the Japanese crypto economy.

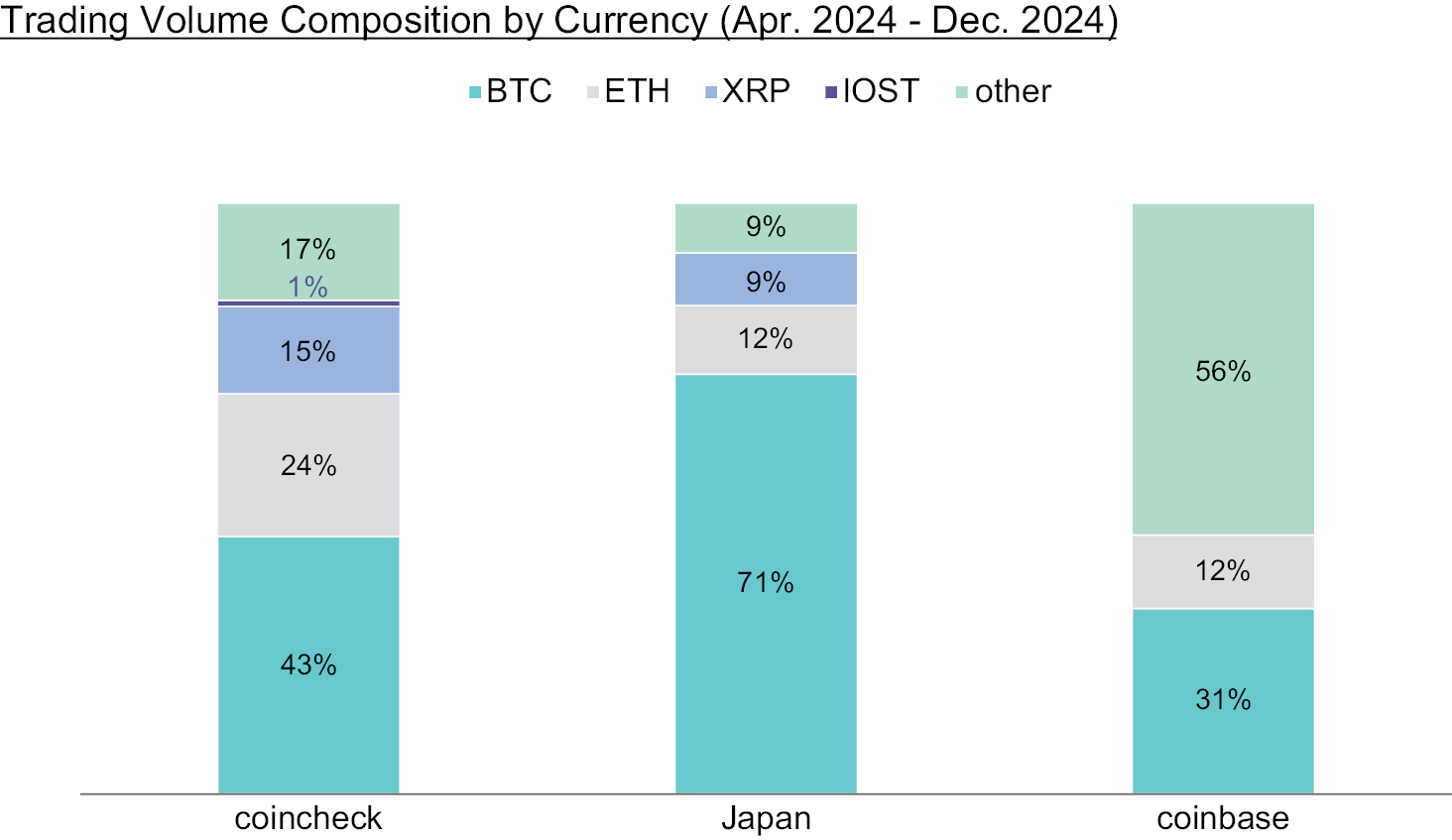

We derive most of our total revenue from trading on our Marketplace platform business. We support trading in 31 different types of cryptocurrencies across all our Marketplace and Exchange platforms as of December 31, 2024. We also continue to be an innovator in the Japanese crypto economy to ensure that Japanese customers and institutions have broad access to the latest technological developments. We conducted Japan’s first IEO during 2021 and have launched a marketplace for NFTs, which we expect to have synergies with our other businesses. Our smartphone application is our main point of contact with our customers, and we believe it provides a user friendly experience with sophisticated UI/UX. To maintain the quality of customer experience we offer, we continuously invest in flexible system and software development, and engineers accounted for 37.1% of our staff as of December 31, 2024.

The Business Combination (as defined below) with Thunder Bridge Capital Partners IV, Inc. (“Thunder Bridge”) has enabled us to access international capital markets, which will help us to finance accelerated growth through increased customer acquisition, additional innovation in crypto asset solutions, and increased opportunities for customers and institutions to more deeply access the crypto economy. Under the Coincheck Parent holding company structure, we have the ability to establish independent subsidiaries focused on crypto asset-adjacent business opportunities. We also have the ability to enhance hiring and retention via equity compensation incentives to further support our competitiveness in our target markets.

We have identified several growth opportunities that may be pursued organically or accelerated through M&A or partnerships, including:

• continuing to grow our customer base and revenue to retain our leading market position, to build on our first-of-its-kind IEO launch and to expand supported crypto asset coverage;

• accelerating our development of NFT platforms in Japan, including by partnering with content creators and gaming companies;

• building new Web3 services supporting the Coincheck crypto asset ecosystem both organically and through mergers and acquisitions;

• capturing nascent and growing institutional interest, capitalizing on our trusted brand name within Japan and in the overall global crypto economy;

1

• continuing to explore new financial service businesses that would appeal to our young customer base, such as payments and commerce enablement; and

• seeking to provide and explore additional on-ramp services between fiat and crypto assets, and various user applications.

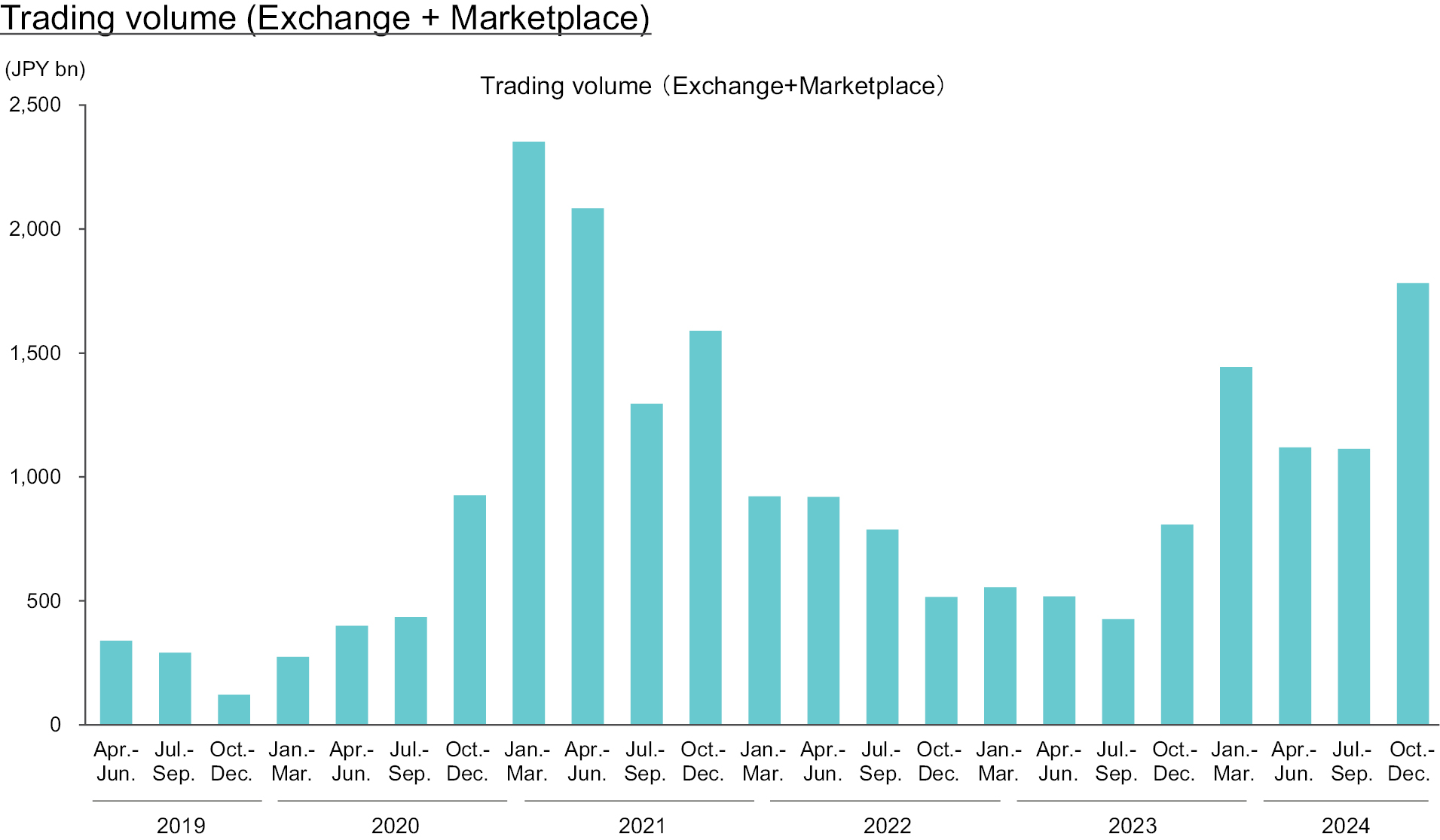

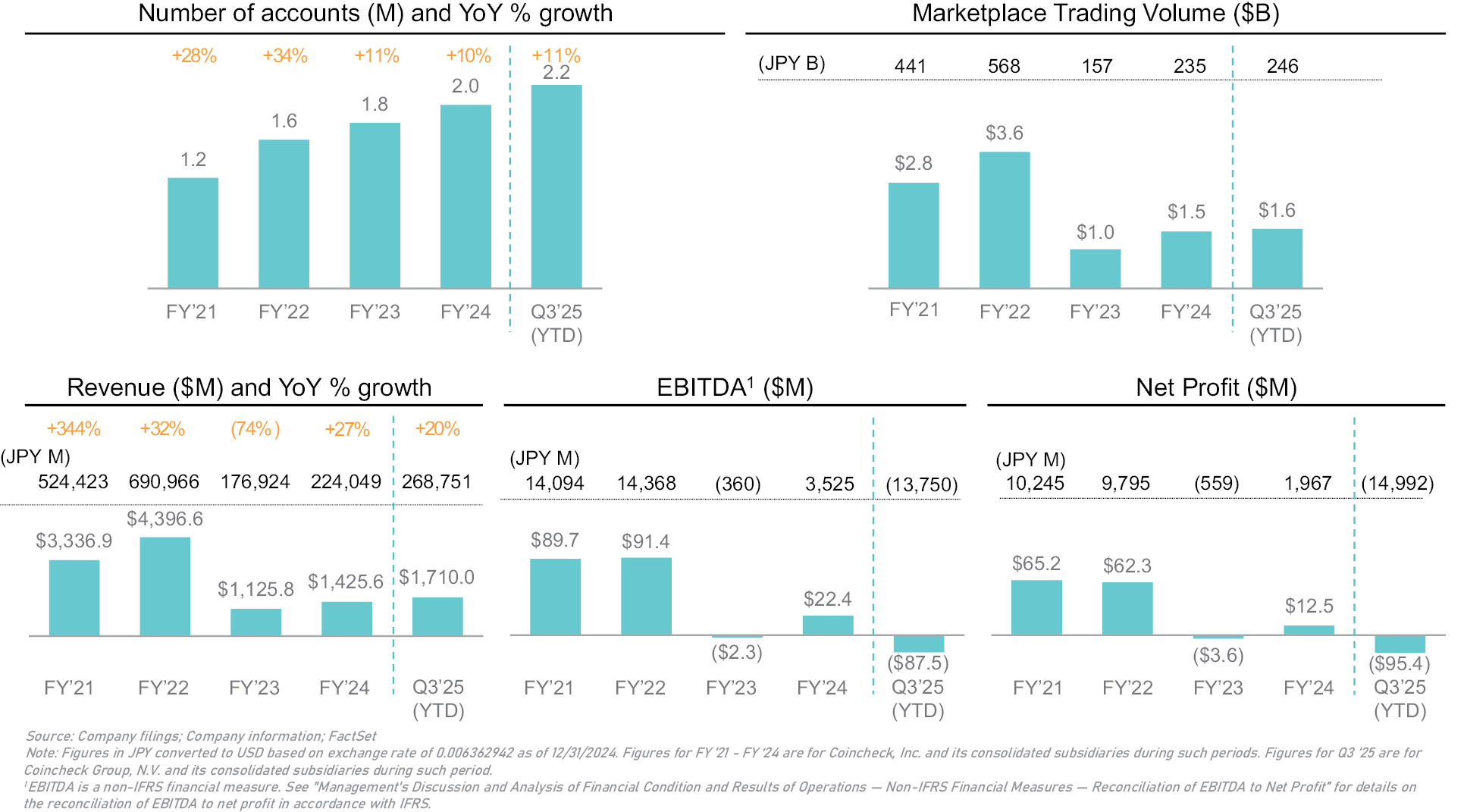

As of March 31, 2022, 2023 and 2024 and December 31, 2024, our customer assets (IFRS) were ¥485 billion, ¥330 billion, ¥708 billion and ¥1,096 billion, respectively. Our marketplace trading volume was ¥568.4 billion, ¥157.1 billion, ¥234.6 billion and ¥245.6 billion during the years ended March 31, 2022, 2023 and 2024 and the nine months ended December 31, 2024, respectively.

Our Mission

Our mission is to increase the accessibility of new forms of investing and commerce for our highly-engaged customer base. With Japan as our first and only current market, we believe that in achieving our mission we will also contribute to the revitalization of the Japanese economy. In pursuit of our mission, we will continue to create crypto asset solutions that enable our users to access and transact utilizing crypto assets and blockchain technologies. Since the launch of our crypto exchange in 2014, we have provided our young, highly-engaged retail customer base with the opportunity to become familiar with crypto assets by offering a service that is easy to use for anyone, regardless of financial or technological literacy.

Our History

After our establishment in 2012 as ResuPress K.K., we launched our crypto asset trading service, “Coincheck” in 2014 and subsequently changed our corporate name to Coincheck, Inc. in 2017.

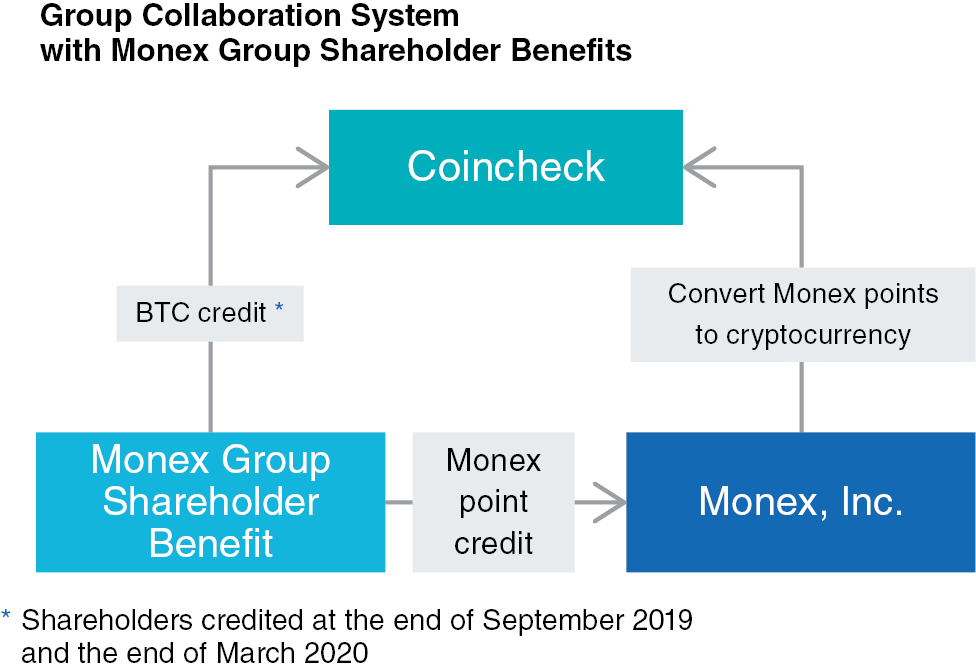

In April 2018, we were acquired by Monex Group, Inc., or Monex, for ¥3.6 billion. At the time of the acquisition, we were implementing ongoing improvements to our security systems to strengthen customer protection and corporate governance through more fully developed risk management systems following a cybersecurity incident in January 2018 in which our NEM hot wallet was hacked and we lost 526.3 million NEM, or ¥46.6 billion, of customer funds. Although we compensated customers who were adversely affected by the cybersecurity incident, we were subject to lawsuits relating to the calculation of the compensation provided. Some of these lawsuits have been resolved by judgment or alternative dispute resolutions but as of December 31, 2024 there is one remaining lawsuit demanding approximately ¥5 million.

In part as a response to this cybersecurity incident, as well as similar hacking incidents that occurred at other cryptocurrency exchanges at around the same time, we joined with the 16 domestic cryptocurrency exchanges in operation in Japan as of March 2018, to form the JVCEA in order to strengthen rules in the industry to prevent future incidents. In October 2018, the JFSA granted the cryptocurrency industry in Japan self-regulatory status, giving the JVCEA the ability to establish standardized operating procedures, including the ability to set guidelines on the crypto assets that may be traded by exchange operators. The JFSA also authorized the JVCEA to monitor and penalize Japanese cryptocurrency exchanges for noncompliance.

After the consummation of the acquisition, Monex worked closely with the JFSA to further implement heightened security measures and better corporate governance. As part of these initiatives, Monex also engaged a financial cybersecurity consulting firm to conduct a holistic review of our processes and system architecture, allowing us to further improve the security of our cryptocurrency exchanges. Under Monex’s control, we also appointed four new directors and three corporate auditors, as well as seven executive officers. These appointments helped to strengthen the supervisory function of the Board of Directors and to improve the independence of auditing matters through the expertise of outside members, and the clarification of this separation of supervision and execution of business matters in order to reinforce our overall management control system. Additionally, we amended our Bylaws in order to transition to become a company that has an audit and supervisory board and created a new management strategy and plan to focus on strengthening our security and governance in order to ensure customer protection and rebuild customer trust. Furthermore, we improved management of segregated customer assets by monitoring such assets on an ongoing basis as well as discussing and reporting them monthly at compliance committee meetings attended by external law firms and full-time audit and supervisory board members.

2

We also improved our risk management policies pursuant to which our risk committee monitors on a monthly basis the state of development and operation of our risk management system as a whole, including by monitoring our financial risk by confirming our positions on a daily basis, monitoring our credit risk by verifying our positions held against a limit amount determined with respect to each cover counterparty, and monitoring our liquidity risk by confirming the supply of each crypto asset and the corresponding number of transactions on a daily basis since October 2018. We also reviewed our risk assessment criteria for crypto assets and amended and restated our criteria for handling crypto assets in February and March 2018, and of the 13 types of crypto assets that were handled prior to the cybersecurity incident, we stopped the handling of four types of crypto assets based on our revised criteria.

In January 2019, after these significant improvements to our risk management and governance systems, we received a license as a crypto asset exchange service provider from the JFSA and registered with the Kanto Financial Bureau under the Payment Services Act. Coincheck is also a member of the Japan Cryptoasset Business Association. We intend to continue to actively work with all of our regulators to improve the regulatory standards of crypto assets in Japan, and Coincheck’s Chairman, Representative Director & Executive Director, Satoshi Hasuo, currently serves as a director of the JVCEA. See “— Regulatory Environment.”

Business Combination

On the Closing Date, Coincheck Group N.V., a Dutch public limited liability company (naamloze vennootschap) (“Coincheck Parent”), consummated the previously announced business combination pursuant to the Business Combination Agreement (the “Business Combination”), dated as of March 22, 2022, as amended from time to time (the “Business Combination Agreement” or “BCA”), by and among Thunder Bridge Capital Partners IV, Inc., a Delaware corporation (“Thunder Bridge”), Coincheck Group B.V., a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) (which was converted into a Dutch public limited liability company (naamloze vennootschap) and renamed Coincheck Group N.V. immediately prior to the Business Combination), M1 Co G.K., a Japanese limited liability company (godo kaisha) (“M1 GK”), Coincheck Merger Sub, Inc., a Delaware corporation and a wholly owned subsidiary of Coincheck Parent (“Merger Sub”) and Coincheck, Inc., a Japanese joint stock company (kabushiki kaisha) (“Coincheck”). Pursuant to the terms set forth in the Business Combination Agreement, (i) Coincheck Parent issued ordinary shares in its share capital (the “Ordinary Shares”) to M1 GK and, pursuant to a share exchange, M1 GK, at that time a wholly owned subsidiary of Coincheck Parent, exchanged all of its shares of Coincheck Parent for all of the outstanding common shares of Coincheck (the “Share Exchange”), resulting in Coincheck becoming a direct wholly owned subsidiary of M1 GK and an indirect wholly owned subsidiary of Coincheck Parent. Immediately after giving effect to the Share Exchange, Coincheck Parent changed its legal form from a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) to a Dutch public limited liability company (naamloze vennootschap); (ii) Merger Sub merged with and into Thunder Bridge on the Closing Date, with Thunder Bridge continuing as the surviving corporation (the “Merger”); (iii) as a result of the Merger, each outstanding Thunder Bridge share sold as part of a unit in Thunder Bridge’s initial public offering (the “IPO” or “Thunder Bridge’s IPO”; each unit, a “Thunder Bridge Unit”; and each Thunder Bridge share, a “Thunder Bridge Public Share”), for the avoidance of doubt, not including any Thunder Bridge Shares held by TBCP IV, LLC, Thunder Bridge’s sponsor (the “Thunder Bridge Sponsor” or “Sponsor”), as of the date of the Business Combination Agreement (the “Sponsor Shares”), was exchanged for one Ordinary Share; (iv) as a result of the Merger, each Sponsor Share was exchanged for one Ordinary Share and (v) as a result of the Merger, each outstanding private warrant exercisable for Thunder Bridge shares (a “Thunder Bridge Private Warrant”) and each outstanding public warrant exercisable for Thunder Bridge shares sold as part of a unit in Thunder Bridge’s IPO (a “Thunder Bridge Public Warrant” and the Thunder Bridge Public Warrants together with the Private Warrants, the “Thunder Bridge Warrants”) became a warrant exercisable for such number of Ordinary Shares per Thunder Bridge Warrant that the holder thereof was entitled to acquire if such Thunder Bridge Warrant was exercised prior to the Business Combination (each such private and public warrant exercisable for Ordinary Shares, a “Private Warrant” and “Public Warrant,” respectively, and, the Private Warrants and the Public Warrants together, the “Warrants”). At the Closing on the Closing Date, the Sponsor forfeited and surrendered, and Coincheck Parent repurchased for no consideration, 2,365,278 Ordinary Shares.

3

The transaction was unanimously approved by Thunder Bridge’s Board of Directors and was approved at the special meeting of Thunder Bridge’s shareholders held on December 5, 2024, or the “Special Meeting.” Thunder Bridge’s shareholders also voted to approve all other proposals presented at the Special Meeting. As a result of the Business Combination, Thunder Bridge, M1 GK and Coincheck have become wholly owned subsidiaries of Coincheck Parent. On December 11, 2024, Ordinary Shares and Public Warrants commenced trading on the Nasdaq Global Market, or “Nasdaq,” under the symbols “CNCK” and “CNCKW,” respectively.

Our Strengths

• We have a leading position in the Japanese retail market.

• We have a young, highly-engaged customer base.

• Our user-friendly platform and product offerings.

• We have a fast-growing product portfolio which is underpinned by robust technology.

• Trusted brand.

• We have a robust and historically profitable financial model.

• Strong and experienced management team to support continued growth.

Recent Developments

Next Finance Acquisition

On March 12, 2025, we entered into a Sale and Purchase Agreement (the “Next Finance SPA”) with the Next Finance Shareholders of Next Finance Tech Co. Based in Japan, Next Finance Tech Co. is a blockchain infrastructure company that provides staking services to a wide range of corporate clients and individual customers globally.

On March 14, 2025 (the “Next Finance Closing Date”), pursuant to the Next Finance SPA, we purchased the Next Finance Shares (the “Next Finance Acquisition”) for an aggregate consideration of ¥265,287,960 and an aggregate of 1,111,450 Ordinary Shares (the “Next Finance Acquisition Shares”). The Next Finance Acquisition Shares were issued in reliance on an exemption under the Securities Act. In connection with the Next Finance Acquisition, we agreed to register the Next Finance Acquisition Shares for resale under the Securities Act and pay all fees and expenses incident to such registration.

The Next Finance SPA provides that, subject to certain customary exceptions, certain of the Next Finance Shareholders may not transfer any of the Next Finance Acquisition Shares during the period beginning on the Next Finance Closing Date and ending on December 31, 2026, provided, however, an aggregate of 70% of such shares will be released from such transfer restrictions at five predetermined intervals between May 14, 2025 and July 1, 2026.

Extraordinary General Meeting

On March 10, 2025, we convened our previously announced extraordinary general meeting of shareholders.

All three of the following proposals were adopted pursuant to a vote of shareholders:

1. Authorization of the Board for a period of eighteen months starting March 10, 2025 to issue up to 25,000,000 Ordinary Shares and/or grant rights to subscribe for such shares (the “EGM Issuance Authorization”);

2. Authorization of the Board for a period of eighteen months starting March 10, 2025 to restrict or exclude pre-emptive rights accruing to shareholders in connection with issuances of ordinary shares and/or grants of rights to subscribe for such shares pursuant to the EGM Issuance Authorization; and

3. Appointment of KPMG Accountants N.V. as the external auditor of our Dutch statutory annual accounts for the fiscal year ending March 31, 2025.

4

Amendment to Non-Redemption and Share Forward Agreement

On March 10, 2025, Coincheck Group, CCG Administrative Services, Inc. (formerly known as Thunder Bridge Capital Partners IV, Inc.) and Ghisallo Master Fund LP (“Ghisallo”) amended and restated the non-redemption and share forward agreement of such parties, dated as of December 4, 2024 (as amended, restated, modified or supplemented from time to time, the “Non-Redemption Agreement”) to among other items: (i) extend the maturity date to March 10, 2026, (ii) adjust the number of Ordinary Shares subjected to the provisions thereof to the remaining balance of 856,242 Ordinary Shares held by Ghisallo, (iii) stipulate that permissible transfers must be at a minimum price of $12.00 per Ordinary Share, (iv) quantify the redemption price of $10.83 per share, (v) release Thunder Bridge as a party thereto, (vi) give effect to the consummation of the Business Combination and (vii) incorporate other conforming and clarifying updates. Pursuant to the Non-Redemption Agreement, if Ghisallo transfers any Ordinary Shares subject to the Non-Redemption Agreement, it must remit the redemption price per share to Coincheck Group (as a recoupment of the payment that Ghisallo received for adhering to restrictions on its Ordinary Shares covered by the Non-Redemption Agreement). On the maturity date, Ghisallo has agreed to transfer to Coincheck Group, at no cost, and free and clear of any liens or encumbrances, any Ordinary Shares subject to the Non-Redemption Agreement and retained by Ghisallo on the maturity date.

Preliminary Estimated Information for January, February and March 2025

The following reflects certain preliminary estimated information for the months of January, February and March 2025, as we disclosed on February 5, 2025, March 4, 2025 and April 2, 2025, respectively, on reports on Form 6-K. The preliminary numbers in the table below are based on information then-available. These preliminary estimates have not been audited by any independent registered public accountants, are subject to update and should not be extrapolated for future periods.

|

January |

February |

March |

||||

|

Exchange Trading Value (Million yen) |

595,094 |

410,135 |

454,277 |

|||

|

Marketplace Trading Value (Million yen) |

46,700 |

25,629 |

19,637 |

|||

|

J-GAAP Customer Assets (Million yen) |

1,285,614 |

873,795 |

859,623 |

|||

|

Number of Verified Accounts |

2,258,295 |

2,278,320 |

2,291,103 |

Notes

• Customer Assets and Number of Verified Accounts correspond to figures as of the end of the month.

• Customer Assets are preliminary figures prepared in accordance with Japanese generally accepted accounting principles (J-GAAP) and differ from the financial figures of the Company, prepared in accordance with IFRS Accounting Standards, and may be revised in the future.

• Historically, Coincheck, Inc.’s total revenue has been derived primarily from transactions on Coincheck, Inc.’s Marketplace platform business. For additional details, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements included elsewhere in this prospectus.

5

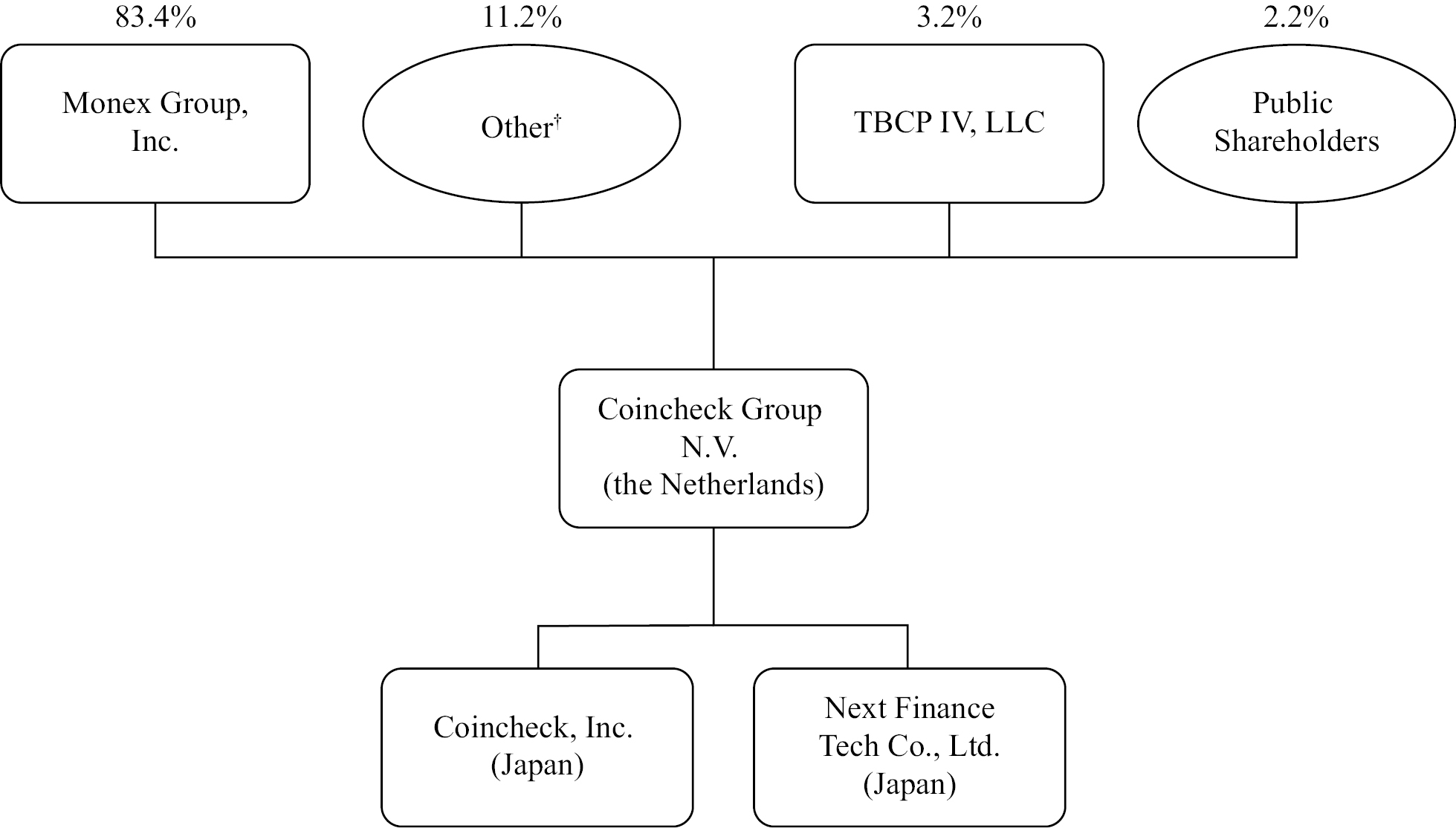

Our Organizational Structure

The following diagram depicts a simplified organizational structure* of the Company and the ownership percentages (excluding the impact of Ordinary Shares underlying the Warrants, Ordinary Shares authorized for issuance pursuant to the Omnibus Incentive Plan and Ordinary Shares held in treasury) as of April 7, 2025. See “Security Ownership of Certain Beneficial Owners” for more information.

____________

* This diagram is provided for illustrative purposes only and does not represent all shareholders or legal entities of the Company.

† Other shareholders, including the founders of Coincheck, Inc and the Next Finance Shareholders. See “Security Ownership of Certain Beneficial Owners” for more information for such shareholders who hold more than 5% of the Ordinary Shares outstanding as of April 7, 2025.

Our Corporate Information

Coincheck Group B.V. was incorporated by Monex Group, Inc. (“Monex”) under the laws of the Netherlands as a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) in February 2022 for the purpose of effectuating the Business Combination and changed its legal form to a Dutch public limited liability company (naamloze vennootschap) and was renamed Coincheck Group N.V. immediately prior to the Business Combination.

Coincheck Parent’s registered and principal executive office is Nieuwezijds Voorburgwal 162, 1012 SJ Amsterdam, the Netherlands. Coincheck Parent’s principal website address is https://coincheckgroup.com/. Coincheck Parent does not incorporate the information contained on, or accessible through, Coincheck Parent’s website into this prospectus, and you should not consider it a part of this prospectus.

Summary Risk Factors

Investing in our securities entails a high degree of risk as more fully described under “Risk Factors.” You should carefully consider such risks before deciding to invest in our securities. Below please find a summary of the principal risks we face, organized under relevant headings.

6

Risks Relating to Our Business and Industry

• Our total revenue is substantially dependent on the prices of crypto assets and volume of transactions conducted on our Marketplace platform. If such prices or volumes decline, our business, operating results, and financial condition would be adversely affected, as well as our share price.

• Our operating results have and are expected to significantly fluctuate from period to period.

• If the utility and usage of crypto assets, the development of which is difficult to predict, do not grow as we expect, our business, operating results, and financial condition could be adversely affected.

• Changes in economic conditions and consumer sentiment in Japan could cause demand for our products and services to be lower than we anticipate.

• Cyberattacks and security breaches of our cryptocurrency marketplace or NFT marketplace, or those impacting our customers or third parties, could adversely impact our brand and reputation and our business, operating results, and financial condition.

• Due to our limited operating history, it may be difficult to evaluate our business and future prospects, and we may not be able to achieve or maintain profitability in any given period.

• The majority of our revenue is from transactions in certain crypto assets, such as Bitcoin, Ethereum or other specific crypto assets. If demand for any particular crypto asset declines and is not replaced by new demand, our business, operating results, and financial condition could be adversely affected.

Risks Relating to Crypto Assets

• Negative publicity associated with crypto asset platforms, including instances of potential fraud, the bankruptcy of industry participants and the violation of applicable legal and regulatory requirements, may cause existing and potential customers to lose confidence in crypto asset platforms.

• Depositing and withdrawing crypto assets into and from our cryptocurrency exchanges involve risks, which could result in loss of customer assets, customer disputes and other liabilities, which could adversely impact our business.

Risks Relating to Government Regulation and Privacy Matters

• Global regulation of crypto assets or crypto asset platforms may develop in ways that limit the potential for growth in usage and acceptance of crypto assets.

• We obtain and process a large amount of sensitive customer data. Any real or perceived improper use of, disclosure of, or access to such data could harm our reputation, as well as have an adverse effect on our business.

Risks Relating to Third Parties

• Our current and future services are dependent on payment networks and acquiring processors, and any changes to their rules or practices could adversely impact our business.

• We rely on third parties to perform certain key functions, and their failure to perform those functions could adversely affect our business, financial condition and results of operations.

Risks Relating to Intellectual Property

• Our intellectual property rights are valuable, and any inability to protect them could adversely impact our business, operating results, and financial condition.

• We may be subject to claims for alleged infringement of proprietary rights of third parties.

7

Risks Relating to Our Employees and Other Service Providers

• The loss of one or more of our key personnel, or our failure to attract and retain other highly qualified personnel in the future, could adversely impact our business, operating results, and financial condition.

• In the event of employee or service provider misconduct or error, our business may be adversely impacted.

Risks Relating to Our Securities

• Fluctuations in the price of our securities could contribute to the loss of all or part of your investment.

• There can be no assurance that we will be able to comply with the continued listing standards of Nasdaq or any other exchange.

Risks Relating to Our Organization in the Netherlands

• We are a Dutch public company with limited liability, and our shareholders may have rights different to those of shareholders of companies organized in the United States.

• We are subject to the Dutch Corporate Governance Code but do not comply with all of the suggested governance provisions of the Dutch Corporate Governance Code, which may affect your rights as a shareholder.

General Risk Factors

• Adverse developments affecting the financial services industry, including events or concerns involving liquidity, defaults or non-performance by financial institutions, could adversely affect our business, financial condition or results of operations, or our prospects.

• Market conditions, economic uncertainty or downturns could adversely affect our business, financial condition, and operating results.

Risks Relating to Tax Matters

• The imposition of additional or higher taxes, whether resulting from a change of tax laws or a different interpretation or application of tax laws, could affect demand for our exchange services and/or may otherwise have a material adverse effect on our business, results from operations and/or financial condition.

• If we cease to be a Dutch tax resident for the purposes of a tax treaty concluded by the Netherlands and in certain other events, we could potentially be subject to a proposed Dutch dividend withholding tax in respect of a deemed distribution up to our entire market value less paid-up capital insofar as it exceeds EUR 50 million.

Implications of Being a Foreign Private Issuer

We report under the Exchange Act as a non-U.S. company with foreign private issuer status. Under Rule 405 of the Securities Act, the determination of foreign private issuer status is made annually on the last business day of an issuer’s most recently completed second fiscal quarter and, accordingly, the next determination will be made with respect to us on September 30, 2025. For so long as we qualify as a foreign private issuer, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

• the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act;

• the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and imposing liability for insiders who profit from trades made within a short period of time;

8

• the rules under the Exchange Act requiring the filing with the SEC of an annual report on Form 10-K (although we will file annual reports on a corresponding form for foreign private issuers), quarterly reports on Form 10-Q containing unaudited financial and other specified information (although we have furnished, and intend to furnish, quarterly reports on a current reporting form for foreign private issuers), or current reports on Form 8-K, upon the occurrence of specified significant events; and

• Regulation Fair Disclosure or Regulation FD, which regulates selective disclosure of material non-public information by issuers.

Accordingly, there may be less publicly available information concerning our business than there would be if we were a U.S. public company. Additionally, certain accommodations in the Nasdaq corporate governance standards allow foreign private issuers, such as us, to follow “home country” corporate governance practices in lieu of the otherwise applicable corporate governance standards. As described in more detail under “Description of Securities — Share Capital — Issuance of shares,” to the extent we rely on such requirements under Dutch law with respect to issuance of shares, our practice varies from the requirements of the corporate governance standards of Nasdaq, which generally requires an issuer to obtain shareholder approval for the issuance of securities in connection with such events. While we do not currently intend to rely on any other home country accommodations, for so long as we qualify as a foreign private issuer, we may take advantage of them.

Implications of Being a Controlled Company

Monex holds more than a majority of the voting power of our Ordinary Shares eligible to vote in the election of our directors. As a result, we are a “controlled company” within the meaning of the Nasdaq corporate governance standards (the “corporate governance standards”). Under the corporate governance standards, a company of which more than 50% of the voting power is held by an individual, group or another company is a “controlled company.”

As a “controlled company,” we may elect not to comply with certain corporate governance standards, including the requirements (1) that a majority of our Board consist of independent directors, (2) that our Board have a compensation committee that is comprised entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities and (3) that our Board have a nominating and corporate governance committee that is comprised entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities. Although we are not currently relying on the exemptions from these corporate governance requirements, if we do rely on such exemptions in the future, you will not have the same protections afforded to shareholders of companies that are subject to all of the corporate governance requirements of Nasdaq. In the event that we cease to be a “controlled company” and our Ordinary Shares continue to be listed on Nasdaq, we will be required to comply with the corporate governance standards within the applicable transition periods or rely on an alternate exemption including those available to a foreign private issuer.

9

The summary below describes the principal terms of the offering. The “Description of Share Capital” section of this prospectus contains a more detailed description of our Ordinary Shares and Warrants.

|

Issuer |

Coincheck Group N.V. |

|

|

Ordinary Shares being offered by us |

Up to 4,860,148 Ordinary Shares issuable upon the exercise of 4,860,148 Warrants |

|

|

Ordinary Shares being registered for resale by the Selling Securityholders |

Up to 127,895,040 Ordinary Shares, up to 129,611 Ordinary Shares issuable upon the exercise of 129,611 Private Warrants |

|

|

Warrants being registered for resale by the Selling Securityholders |

Up to 129,611 Private Warrants |

|

|

Terms of the Offering |

The Selling Securityholders will determine when (subject to compliance with the contractual lock-up restrictions that apply to certain Selling Securityholders) and how they will dispose of any Ordinary Shares and Warrants registered under this prospectus for resale. The Selling Securityholders may offer, sell or distribute all or a portion of the securities registered hereby publicly or through private transactions at prevailing market prices or at negotiated prices. See “Plan of Distribution.” |

|

|

Warrants issued and outstanding |